Housing Affordability Needs a Workforce and Investor Restrictions

Housing Affordability Needs a Workforce and Investor Restrictions

Without accounting for the workforce shortage and the impact of investors on existing and new supply, housing will be a permanent issue

Introduction

On June 23rd, 2022 the Canadian Mortgage and Housing Corporation (CMHC) published its report, “Canada’s Housing Supply Shortage: Restoring affordability by 2030”, (the Report) calling for an additional 3.5 million housing units in order to achieve affordability for Canadians. The Deputy Chief Economist called for “an ‘all-hands-on-deck’ approach to increasing the supply of housing to meet demand.”

This is useful and needed. When millions of Canadians are having their lives limited because of how much shelter costs it is absolutely worthy to make affordability a goal. In Maslow’s hierarchy of needs, shelter sits right next to water and oxygen. If you were to wash up on a deserted island, creating shelter would be a first-order priority.

The absence of affordability, or poverty, is a prime indicator of health and mental health issues. Only recently we learned that a woman suffering the effects of Long Covid is working through the process of Canada’s Medical Assistance in Dying (MAiD) program. ““[MAiD] is exclusively a financial consideration,” she told CTV News Toronto.”

Without support, she feels her options are limited. Even if she did qualify for disability assistance, the maximum amount would barely cover rent. Beginning on March 17, 2023, applicants with a mental illness as their sole underlying medical condition will qualify for MAiD in Canada.

Given that poverty is a major social determinant of mental health this seems particularly cruel.

One MAiD practitioner told CTV, “We have to be careful we don’t apply laws that inadvertently help people terminate their lives because they don't feel valued or respected or that they belong”.

The woman at the centre of the article concluded, “The government as a body is telling people that they're willing to assist them to death because they don't have enough money to live with dignity. That is a pretty clear signal to me that, unless you are able-bodied enough or able-minded enough to work to produce profit, then you don't have any place here.”

This paradox of a society compassionate enough to allow people to die in dignity but not live with dignity is vicious in its morality. As rental rates rise despite falling housing prices, and as cost of living and inflation impact everyone but not everyone equally, there is a clear call for the government to step up and act in the long-term public interest.

CMHC’s call for 3.5 million additional units by 2030 might be the clearest goalpost and timeline by an official body. When we use 3.5 million homes by 2030 as our goal date, we can break down how feasible it is to accomplish using existing measures and data.

But when we do so, we find that while CMHC is good at articulating its supply and demand approach, it heavily favours new-supply-side solutions while skirting the impact of investors and the workforce shortage.

Investors make up at least one-fifth of home purchases, and there is an expected shortage of thousands of skilled trades workers over the next several years.

It might be helpful to take a hypothetical community with X number of people in it, and Y number of people who are in Core Housing Need, defined as unsuitable or unaffordable housing without affordable alternatives, and Z number of people moving into the community every year.

How many homes are needed to make housing affordable for everyone? How many are built each year? When will housing become affordable?

If your rate of new housing supply is constrained by not having enough workers, the demand for affordable housing may always be beyond supply. Prices go up as there are more people who need or want a finite amount of product.

And if demand includes people who are buying second, third, or fourth homes, whatever new housing does trickle out the conveyor belt will have investors waiting to make a return on one of Maslow’s basic needs.

Even excluding the impact from population growth or short-term rentals or empty homes or money laundering, but just focusing on workforce and investment shatters any feasibility to building enough new supply to outcompete demand.

If governments fail to account for Canada’s workforce crisis and the impact of investors buying up new and existing supply, the logic of supply and demand stops being met by reality and instead becomes more like a belief system.

Ultimately this will make affordable housing a permanent election issue, which it arguably already is.

What follows is an evaluation of the claims and assumptions by the CMHC and others that the answer to the housing crisis is to simply “build more”. When we quantify that we discover pain points that are too often dismissed or diminished in favour of barriers to approving new projects.

The wrong goals are being measured in Housing Starts, and the housing crisis gets worse over time. No one has a crystal ball on how a recession will impact the housing market. When cities have seen 60-70% increases over a few years and a recession peels back 50%, will average Canadians suddenly be ahead when interest rates are much higher and job prospects might be dimmer? Or could Canada see a similar situation as happened after the US financial meltdown in 2008, with cash-rich institutions stepping in as millions of Americans lost their homes to foreclosure?

No one can say for sure, but what we do have is the CMHC report and the long-suffering calls for new supply to compete with demand.

Supply Demands a Workforce

Demand for more housing rests on a logic that more supply will compete with and outpace demand, cooling prices. In one example, an Op-Ed in the Hamilton Spectator written by the CEO of a development company:

“...[H]ousing starts are not keeping pace with population growth…You can only build your way out of a housing supply shortage. Endless processes, outdated regulations and restrictions make it nearly impossible to build homes at the rate we know we need. Red tape, high taxes on housing and government-imposed restrictions are chocking [sic] the housing supply chain, be it newly built communities, missing middle housing options like townhomes and triplexes, or high-density housing on transit.”

That could all be true and none of it would matter if there isn’t a workforce to build it.

BuildForce Canada, a data holder for construction sector labour information, estimates that Canada will be short 27,000 skilled workers by 2027 even with enhanced recruiting from immigration.

There is no quick fix to this either.

The CEO of Vancouver Island Construction Association said in 2021 about labour shortages amidst the pandemic housing boom, “It's at that state where we want to do something now. And if we want to avoid that truly critical state in five to seven years, we need to start making some inroads now to expand our trade workforce."

Workforce development begins years in advance, ““We have to start presenting the skilled trades to young people earlier in their education journey and creating a system that allows them to excel at shop and makes them a vocational rock star when they graduate," [CEO Rory Kulmala] said.”

The Vancouver Regional Construction Association (VRCA) estimates a current shortage of 7,300 skilled trades with thousands more over the next several years.

The BC Construction Association estimates 11,331 construction jobs will be unfilled in the province by 2030 due to labour shortages.

Alternative sources of labour, such as through immigration and foreign workers is possible, but there is a lag and labour mobility issue that has to be surmounted.

Demand for Housing as Commodities

A Bank of Canada analysis on housing demand found that one-fifth of all mortgages were by investors. This analysis, with limitations such as excluding mortgages financed from outside their list of institutions or purchases made with cash or by corporations, found that since 2014, “even under these parameters” at least 19% of purchases were by investors.

The “financialization” of multi-family properties, as found by University of Waterloo Assistant Professor Martine August and published in 2020 in the Journal of Urban Affairs, found that since the 1990s, Real Estate Investment Trusts (REITs) had total asset values of $80 million in 1993 ballooning to over $75 billion in 2019 (August, 2020, pg. 980). This growth largely occurred by consolidated existing stock, not through new development.

According to August’s findings, in 2017 the top 25 REITs held 290,712 units. Total ownership of the top 25 landlords, including private and family-run companies, was 352,910 units.

Over the pandemic the assets held by REITs has grown.

One company, Starlight Investments, was reported in 2017 to possess 26,221 housing units (August, pg. 981). According to Starlight’s investment page today it has over $19bn in Canadian multi-family residential assets under management and over 61,000 housing units.

Investors may be a part of the housing ecosystem but their stake involves leasing one of Maslow’s basic needs for a return.

When a building or suite becomes an asset, returns are approached in two ways: reducing expenses or raising revenues, i.e. rents. Avoiding repairs could reduce expenses while enforcing strict rules around rent dues, regardless of extenuating circumstances, enables turnover at higher rental rates. This was enabled by deregulation of vacancy controls as happened in Ontario in 1997, allowing rent increases of any amount upon turnover (August, pg. 979-80).

From the Vancouver Sun, “Starlight has highlighted their business model in other markets, through their own materials and regulatory filings, the Globe and Mail reported in November, including a 174-unit Toronto rental building they’d acquired where they increased average rents by $411 a month over four years.”

The commodification of shelter has created investor demand above and beyond normal population growth, which is a mix of natural growth (births minus deaths) and immigration.

Investors by definition are not “in Core Housing Need”. And if investors use the logic of supply and demand on top of their obvious interest to make returns they will continually be upping rents until presumably, more supply is added to outpace demand, thereby increasing “choice”, tilting bargaining power back to homeowners and renters and reducing growing rent prices.

Using the justification of “competitive market” pricing enables landlords to charge exorbitant amounts on the knowledge that someone somewhere needs this product enough they will pay. The invocation and practice of “competitive market” pricing has been called barbaric and mean-spirited when it was used for hand sanitizer and toilet paper at the start of the pandemic. But this is shelter. Shelter is as needed as oxygen and water.

This construes a sort of collectively accepted profiteering that will continue until supply puts bargaining power back into the hands of renters.

But this assumes Canada has enough workers who can build enough to not only meet demand from population growth but also demand from investors. A recent Motley Fool article republished by Yahoo Finance, presents REITs as an investment opportunity to watch over the current market decline on the basis that,

Even though it’s a residential REIT and may experience a harder impact from the housing market decline compared to commercial REITs, it might not be as bad as you might think. Even if the company experiences a devaluation of its residential assets, its finances rely upon rent.

And as long as the rents don’t see a decline proportional to the property prices, there might not be a significant enough dip in the REIT’s earnings.

Better Dwelling, while not clearly showing its sources and math, claims as many as 39 and 44% of new homes built since 2016 are purchased by investors in Toronto and Vancouver, respectively.

Housing Wealth is Concentrated

Housing is also being hoarded by the well-heeled. Statistics Canada (StatCan) found the top 10% of individual income in Canada accounts for a quarter of total residential housing wealth, with owners of multiple-properties holding at least a third of all residential properties.

Echoing August, complexities with data collection and reporting make finding out who owns how much of what far from simple and likely undercounts. In her paper, in 2017, the top 25 REITs held 18% of all Canadian privately initiated apartments in buildings with over six units. Between 2011 and 2017 the proportion of suites owned by the top 20 landlords increased 27.8% while the number of apartments grew by only 6.5% in that same period (August, pg. 980).

To continue using BC as an example, there are over 2 million occupied private dwellings in the province distributed between 1.768m properties including 207,315 properties with multiple residential units (i.e. duplexes and apartment buildings).

The Canadian Press wrote in April 2022 and widely syndicated since, that 15% of Property Owners hold 29% of housing stock in BC. Note the use of “housing stock” here.

What StatCan published: “In Nova Scotia, New Brunswick, Ontario, and British Columbia in 2020, these owners held between 29% (British Columbia) and 41% (Nova Scotia) of the property stock while accounting for 15% (British Columbia) to 22% (Nova Scotia) of owners.”

Under StatCan’s Note to Readers: “property stock refers to all residential properties in a province or territory, including vacant land, within the target population of the Canadian Housing Statistics Program (CHSP).”

This effectively means StatCan is not saying one-third of housing is owned by 15% but that of the total residential properties, 29% in BC is owned by 15% of homeowners.

Housing stock refers to all dwellings, including those in apartment buildings, which one building with multiple residential units make up one residential property.

Other limitations to data allude to much higher concentration of housing wealth: data is only available for some provinces and not all:

In this release, people who own multiple residential properties are those whose name is on the property title of more than one residential property within a given province or territory. For the purposes of this release, people who own one property in a given jurisdiction and a second property in another jurisdiction are not included among multiple-property owners at this time. [emphasis added]

This does not say that someone whose primary residence is in Alberta and owns multiple properties in BC would be counted (and Alberta isn’t included). The data above also does not include non-individual property owners, meaning mostly corporations.

According to this StatCan table, in BC in 2020 there were 210,985 property owners of a single property with multiple residential units, and 51,245 of those owners held multiple properties with multiple residential units, including duplexes and apartment buildings.

This table shows 79,605 individual owners of three or more properties with the average number of properties owned being four.

Customizing the same table, the number of non-individuals (mostly corporations) with those owning three or more properties hold an average of 20 properties with an indeterminate number of dwellings.

The StatCan table customized and pasted below shows how many corporations own property titles of various property types in BC in 2018, the available year for data.

10,310 properties with multiple residential units are owned by corporations.

To try and cross-reference this, the BC Land Title and Survey state that altogether there are 2.2 million active property titles (residential and other) as well as 33,871 active strata plans and 720,538 active strata lots.

The number of strata plans roughly tracks with the number of strata condominium apartment buildings in 2018.

Putting all this together, it seems one-third of housing concentrated in the hands of very few is likely an underestimate.

However, CMHC’s report is silent on this when talking about existing supply and focuses instead on the creation of new supply.

Calculating Out Supply & Demand

The CMHC report estimates the number of homes in Canada will increase at current trajectory to over 18 million by 2030. They then establish a process for arriving at 3.5 million homes would be needed in addition to this for housing to reach a level where shelter costs 40% of disposable income per household.

Laid out on page 23, the report envisions if the goals of increased supply can be met that the average home prices in Ontario to fall to between $499-$551,000. For BC, the average home would be between $607-$679,000.

The report says Ontario needs to build an additional 1.8 million homes while British Columbia needs an additional 570,000. This would work out to Ontario needing 257,000 additional homes built annually for the next seven years while BC would need 81,000 for its part.

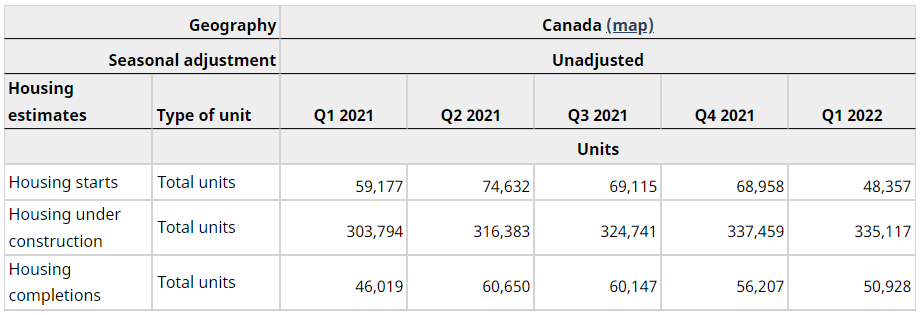

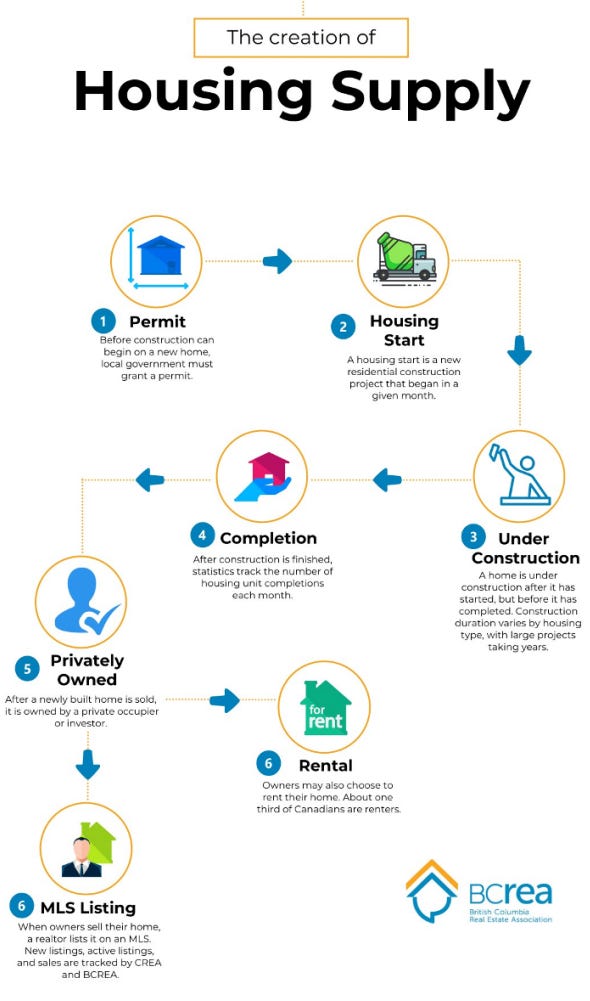

To gain a sense of how much supply is currently being added, StatCan and CMHC collect and report out three categories of housing data: Starts, Under Constructions, and Completions.

Housing Starts means homes that are approved, registered, and the shovels have broken ground. Completions means homes that are ready or near ready to live in and be absorbed by the market. Under Constructions understandably means by the next time the survey is taken the new homes started are in-progress.

In terms of numbers we can look at the data published by StatCan and shown below. Starts and Completions run roughly parallel while Under Constructions is about five times higher than both.

To better visualize this and show the relationship between each, the below is borrowed from the BC Real Estate Association (BCREA) and its report on supply-side policies for the BC housing market (pg. 3) :

In calculating the annual averages for each housing category for Canada between Q1 2018 and Q1 2022 there were:

191,929 average new homes started each year

958,267 average homes under construction in a given year

170,030 average new homes completed or near complete each year

This suggests there is a physical cap to how many homes how fast can be built.

Ontario built 90,000 homes in 2021, according to Mike Moffatt, senior director at the Smart Prosperity Institute, but the 750,000 homes projected to be built by 2030 would need to see an additional 1.85 million for the average home price to fall between $499-551,000. But there too exists a workforce shortage.

In 2021, BC completed 41,000 new homes. The annual average over five years is about 36,000.

If we assume from now on BC completes 41,000 homes each year it would take nearly 14 years to complete 570,000, not including the status quo projected numbers.

The CMHC explains the housing crisis as “Overall, the loss of affordability can be attributed to a housing supply not responding to demand in some of Canada’s large urban areas over the last 20 years.”

And to solve it, “we need an ‘all-hands-on-deck’ approach” including developers making full use of land holdings, “partnerships and innovation” to increase housing supply, and all levels of government to “help build supply”.

And this is largely measured in Housing Starts. The Op-Ed quoted earlier references Housing Starts when urging action on the housing shortage, but Starts tracks the rate of homes approved and shovels breaking ground.

Housing Starts versus Completions

Housing Starts are the official barometer of construction sector activity but the distinction seems vital. Completions is a tangible measure that at least somewhat reflects the physical capacity of the workforce to build homes. So while Starts and Completions are nearly identical in number each quarter and each year, far more articles and returns exist for Housing Starts (405,000 returns as of writing this) than Housing Completions (19,600 returns as of writing this).

The BCREA includes Starts in their quarterly housing forecasts (page 14 typically) but very rarely mention Completions unless incidentally in their columns.

If the housing crisis is about not enough real-world homes actually able to be lived in at a rate that brings down prices, then why wouldn’t something like Housing Completions be used?

It feels outdated, and seems to enshrine improving Housing Starts and not Completions.

A New-Supply-Side Worldview

To further explore the CMHC report’s understanding of the housing crisis, the report “found that demand for housing grew with higher incomes and population growth, and long-term declines in interest rates.” Further:

Our analysis shows that affordability is an inherent challenge in modern economies. As house prices grow, our statistical results show that demand for housing would decline only marginally across Canada. In contrast, as incomes grow then demand for housing shows large growth. This combination of more demand as incomes grows but negligible decline in demand as prices grow will lead to affordability being an inherent challenge in a growing economy. Unless, that is, we have more housing supply.

When economists use “inherent challenge in modern economies” that typically means there’s a worldview at work. This deserves some level of scepticism.

Recall that Alan Greenspan, Chair of the Federal Reserve had famously said his model of “how the world works” had a flaw:

I made a mistake in presuming that the self-interest of organisations, specifically banks, is such that they were best capable of protecting shareholders and equity in the firms ... I discovered a flaw in the model that I perceived is the critical functioning structure that defines how the world works. I had been going for 40 years with considerable evidence that it was working exceptionally well.

When CMHC calls the housing crisis, which is also happening in places like New York and Los Angeles and Seattle and San Francisco and Sydney and Boise and Markham and London and Miami an “inherent challenge”, that presumes the wealth inequality and corporate hoarding and housing injustice is an inevitability in “modern economies”.

How is that not a worldview?

The United Nations released a statement in 2019 that private equity and investment firms have “transformed the global housing landscape by raising rents and forcing some tenants out of their homes.” The UN Special Rapporteur cited the business practice of classifying affordable housing as “undervalued” and the weak state of tenant protections in many jurisdictions as directly contributing.

Which of this is an inevitability of modern economies?

The CMHC Report continues:

With concrete and credible actions to increase housing supply however, such expectations would decline and reduce growth in demand for housing. Such credibility could be enhanced by firm commitments to ambitious increases in housing supply and regular and transparent reporting on how much housing is in the process of being approved, planned and started. (pg 13)

Increase supply. Approve it, plan it, start it. But what about completing it?

In discussing the barriers to achieving 3.5 million additional homes by 2030, CMHC’s report only briefly mentions the workforce shortage, couched somewhat awkwardly in presumptive language:

Currently, skills shortages and supply-chain challenges are pushing up construction costs—meaning it can take more time to build. Dramatically and suddenly increasing the supply of housing will put pressure on the costs of construction so planning on increased supply needs to take place now. But the construction sector needs to become more productive as well because its productivity growth has been low in relation to the rest of the economy.

These challenges in construction are layered on long-standing challenges of progressing through the regulatory system to get new housing built. It can take many years to obtain approval for new construction in some parts of Canada. Without any means of lowering Canadians’ demand for housing, increased housing supply is the only means of achieving affordability. (pg 7)

Look at just two sentences from this: “The construction sector needs to become more productive as well because its productivity growth has been low in relation to the rest of the economy.” Who is this important to other than economists?

“Increased housing supply is the only means of achieving affordability.” Great. How do we get there in a way that demand is met and outpaced when there is a skills shortage?

A central assumption CMHC has is thinking increasing supply improves affordability.

CMHC writes, “How will supply improve affordability? More housing units created in the housing market will create opportunities for households to move into housing that responds to their demands. In addition, this ‘filtering process’ likely frees up housing to improve housing affordability over time. (pg 6)”

This is what is meant by belief system. An otherwise robust logic not met by reality but still adhered to and doggedly pursued is a belief system.

If not enough supply can be built to outpace population growth and the investors in major cities where most of the identified housing is needed, then regardless of how much focus is on removing barriers to development demand will always outpace supply.

This belief that removing those barriers will solve the problem is also shared by the private sector. Like the Op-Ed earlier,

You can only build your way out of a housing supply shortage. Endless processes, outdated regulations and restrictions make it nearly impossible to build homes at the rate we know we need. Red tape, high taxes on housing and government-imposed restrictions are chocking [sic] the housing supply chain.

Without articulating the rate of supply against the rate of demand the solutions write themselves to focus on improving Housing Starts.

CBRE, a commercial real estate and investment corporation, concluded in their 2021 annual report that, “The policy-based barriers restricting the development of new rental housing will continue putting demand on the rental market [and] continue to put downward pressure on vacancy rates and upward pressure on rents.”

“Upward pressure on rents” occurs because more people want a finite supply and are willing to pay more, but only because the people renting out one of Maslow’s basic needs recognize that those with more will pay higher for what they own and rent out. Higher rents could alternatively be pinned on “competitive market rate” or inflation.

A Logic Model versus a Belief System

But using CMHC’s and so many other’s logic we have to throw enough supply at the problem to turn it around.

This is deeply flawed. At worst, it may just be used to push for more development that sacrifices food security, farmland, greenspace, and social concerns to build out unsustainable cities of expensive shoeboxes.

Food shortages are real. Supply chains are fragile. Wars and droughts in far-off places impact us here in Canada.

Even if local governments do everything they can to speed up approvals, even if the provinces overrule municipalities on greenbelt and agricultural land uses, maximum heights, intensity and density, even if municipalities magically amalgamated and automatically approved all the biggest proposals, the workforce remains the bottleneck.

And investors sit maws agape at the end of that conveyor belt.

There is not a lot of room for optimism that new supply will ever outpace its constraints or the factors of demand.

The CMHC report also calls for governments to “help by subsidizing housing costs for low-income Canadians (pg 5)”.

You would think this is until enough supply can be built to outpace demand, but on the publication release webpage, CMHC wrote, “It’s important to note that even if we do reach these targets, there would still be many low-income households that would face affordability challenges.”

So what are we even doing here?

When rental buildings are bought at record-breaking numbers in 2021 by Real Estate Investment Trusts (REITs) and we know that these companies are actively finding ways of delivering greater returns for their investors, who exactly is being subsidized here? Arguably not tenants.

The CEO of Starlight Investments was quoted saying: “We think there is a definite housing shortage, or almost a crisis level in Canada … and the good news for investors is there is no easy solution in sight. … This is not good news for consumers.””

But the CMHC report insists, “achieving housing affordability for everyone in Canada will be done with increasing supply in the rental and homeownership market, and having this supply respond more quickly to greater demand. (pg 5)”

Without quantifying “greater demand” and its impacts, how can we be sure with any certainty that increasing supply will outpace that demand?

Remember, if the goal by 2030 is for British Columbians to be able to buy the average house for between $607-679,000 that may still be beyond what many find affordable or within reach. And that is after building an extra 81,000 homes each year.

British Columbia in 2021 had 41,000 Housing Completions. It would need to build more than 122,000 housing units every year starting 2023.

The BCREA and real estate boards as well as the CMHC continue to advocate supply-side policy changes but are relatively quiet on meaningful solutions addressing the workforce or the concentration of housing wealth by investors. One such real estate board president said “When I’m talking to the media I sound like a stuck record – I bring everything back to supply. But unfortunately, that’s our answer”.

The answer to what?

The BCREA flirts with the reality of workforce constraints in their report “Bigger, Faster… More Affordable? Evaluating the Impact of Supply Side Policies on the BC Housing Market” released May 2022:

Regulations related to permits and starts are certainly an obstacle to housing supply. However, the surging ratio of workers per unit under construction may suggest that there are also capacity constraints in the development industry, even after a project is out of the hands of city planners. Examining the ratios across all provinces, we observe a downward trend.

Whether the types of improvements modeled in our research are achievable is outside the scope of this Market Intelligence, although the section on construction labour markets suggests building more may require expanding the labour supply in addition to regulatory and zoning changes.

CMHC in concluding remarks:

These are big numbers, but the task of restoring affordability is also huge.

Ensuring housing affordability for everyone in Canada is critical to Canadian families and the economy at large. The federal government cannot achieve affordability for everyone in Canada on its own. We need partners. The private sector will be critical in addressing this supply shortfall.

For their parts, governments can help by ensuring that the regulatory process is as efficient as possible while respecting important environmental and social concerns. (pg. 27)

Solutions Aren’t Generated in a Vacuum

The solutions posed by the biggest partners of the government on the housing crisis seem to be disproportionately aimed at solving the problem of low Housing Starts. In other words, once a project is approved, that is guaranteed future income for developers and realtors.

This is a massive blind spot for policymakers and the public alike.

Housing Completions is not only a better measure of tangible new supply, but would at least get at the bottleneck of the workforce and the individuals and corporations gobbling up what trickles through.

People are desperate for affordable housing, creating a demand for a supply of promises by politicians and political parties at every level. This will either be delivered, under-delivered, or not delivered at all between elections. Feasibility about how and where this supply comes from is critical.

No one can say for certain what will happen if a recession craters the housing market if it does at all. When the average price increases some 70% then decreases 50% that may not be what median-income individuals find affordable, particularly when interest rates are higher and job prospects are dimmer.

No one can say if all those investors would sell off their assets too, flooding the market with supply. Or if only some of them would sell some of their assets? Would regular folk be able to get in on the housing market then? Would vulture capitalists and cash-rich institutional investors step in? What happens to rents if development companies go under between Housing Starts and Completions?

Nobody has the crystal ball on that.

We do not need to attach a malicious or sinister agenda to why the focus has been on essentially better guaranteeing returns for developers and realtors and investors. Nobody is a bad guy in their worldview. This can be explained instead as simply a frailty of our political moment.

The likely truth is that housing is a systemic problem in need of a systemic solution, but like many of the wicked problems facing society like healthcare and clean energy and climate change, the implications on our political economy are too much to ask of our political culture.

Wealth taxes to fund purpose-built rentals and affordable housing, to remake healthcare from the ground up and train a workforce, or to rebuild crumbling infrastructure is simply beyond the ability of Canadian (or American or British or Australian) political problem-solving.

In Overton Window or Hallin’s Spheres terms, radical action that imposes harsh restrictions on investors, or forces a three residential property maximum on the wealthy, or forbids corporations from trading much-needed shelter as commodities, is deviant thinking. Impossible. Pie-in-the-Sky. Get real.

So instead, popular discourse is a buffet of solutions conveniently if unknowingly catered to avoiding imposing restrictions or taxes on investors, corporations, and the elite. This discourse is engaged in public forums online and off, on platforms like Facebook and Reddit’s r/CanadaHousing.

The solutions in good currency, often informed by witnessing and engaging and absorbing discourse in peer groups and families and online, show what is possible in people’s minds enough that they are a voting bloc to cater to with party messaging during elections.

Like the CEO of the development company said in the title of his Op-Ed, “Demand action on housing through your vote”.

If what works to fix the housing crisis is “too radical” for either politician or public, that attitude does not exist in a vacuum. “All-hands-on-deck” might just mean looking at existing supply concentrated in the hands of investors and speculators and forcing them out to inject ready-to-go supply into the market. It could mean public options for building housing when a recession slumps the industry.

Reintroducing the idea of publicly-funded social infrastructure projects may be essential and could address more than one problem. Both Federal and provincial governments used to be more directly involved in creating housing. That stopped beginning in the 1980s when it was assumed the private sector could shoulder the responsibility better.

Years of that logic not being met by reality has compounded the housing shortage into a housing crisis, and now has been punctuated by a pandemic and supply chain disruption and the unanticipated effects on demand.

More Supply to the Right People and No One Else

New housing will likely be essential to dealing with the housing crisis, and so the concerns about approval processes are validated. The CMHC states that in BC it takes 18 months to get from initial proposal to permits and shovels breaking ground.

But outside the realm of polite discussion is forcing restrictions on investors and corporations, despite clear concentration of housing wealth. Outside the realm of discussion is massive workforce development paid for by taxes on the economically and politically powerful. That may have to change if the answer is supply.

Existing supply hoarded by the well-heeled, kept either empty or rented out at exorbitant “competitive market” rates are part of the equation of supply and demand, but are not part of the conversation in any serious way about solving the housing crisis.

If the answer is more supply, then it is “more supply [new and existing], the right supply [diversity of options], to the right people [individuals, not corporations], and no one else [no investors/before investors]”.

Maybe then illness compounded by Core Housing Need in people’s lives wouldn’t nudge people to assisted suicide. But it takes a shift in political culture and the ideas of what is possible as solutions to public problems for this to occur.

Works Cited:

Martine August (2020) The financialization of Canadian multi-family rental housing: From trailer to tower, Journal of Urban Affairs, 42:7, 975-997, DOI: 10.1080/07352166.2019.1705846